Read summarized version with

In 2024, the CFO of a Hong Kong-based multinational joined a video call with colleagues: the CEO, the CFO, several familiar faces. They discussed an urgent wire transfer. He authorized it. The total: USD $25 million. Every person on that call, except him, was a deepfake. This wasn’t a niche attack on an obscure company. It was a proof of concept and it has since been replicated across industries worldwide, including financial services.

Canadian banking is not insulated from this reality. According to a recent Canada survey, 81% of Canadian organizations experienced attempted or successful AI-powered fraud in the past twelve months. Sixty percent fell victim to fraudulent communications using AI agents or AI-generated content. Twenty-four percent were hit by voice clone attacks. And 72% of those targeted were hit more than once, because the attacker learned from the first attempt and adapted.

“What we’re seeing in our work with Canadian financial institutions is that the threat has moved faster than most organizations’ mental models of it,” says a Senior Dedicatted consultant specializing in financial crime prevention. “Leadership teams are still thinking about fraud as something that looks anomalous. The most dangerous attacks today look completely normal, until the damage is done.”

The financial industry globally still detects only about 2% of financial crime flows, despite increasing compliance spending year over year. And with FINTRAC, OSFI, and the advancing provisions of Bill C-27 demanding more accountability than ever, the pressure is arriving from every direction at once. The question for Canadian banking leaders is no longer whether AI fraud detection is worth the investment. It is whether your institution is deploying it with the sophistication the threat now demands.

The Industrialization of Fraud: How AI Has Changed the Threat Landscape

What makes today’s fraud environment categorically different isn’t just the technology – it’s the economics. For most of financial crime’s history, sophisticated fraud was expensive to execute. It required skilled operatives, significant preparation time, and manual effort that naturally limited scale. AI has dissolved all three constraints simultaneously. The same machine learning tools, the same large language models, the same automation capabilities available to your technology team are available to the people targeting your institution, often deployed faster, with fewer governance hurdles, and at a fraction of the cost. The result is fraud that is highly personalized, adaptive, and cross-channel by design. Four threat vectors are hitting Canadian banks hardest right now

Synthetic Identities

They have become AI’s most insidious contribution to financial crime. These aren’t crude fake IDs – they are fully realized digital persons, internally consistent across names, addresses, Social Insurance Numbers, credit histories, transaction behaviours, and social media presence. AI generates them in minutes. They are then carefully nurtured over months: small accounts opened, modest transactions made, credit limits incrementally increased, credibility established. Then, in what the industry calls a “bust-out,” the synthetic identity rapidly exhausts every credit facility it has built and disappears. Canadian institutions often don’t discover the loss until well after the account is closed and by then, the same identity factory has generated hundreds more.

We worked with a mid-tier Canadian lender that had been approving a cluster of applications that looked, individually, completely clean. Good credit scores, consistent employment history, reasonable loan amounts. It was only when we mapped the relationship graph: shared devices at application, overlapping address histories, coordinated drawdown timing, that the pattern became visible. Traditional rule-based systems never would have caught it because no single application broke any rule.

Deepfake social engineering

It has moved from theoretical concern to documented operational reality. Voice cloning technology is now accessible enough that a few minutes of audio from a public earnings call, an investor presentation, or a media appearance is sufficient to generate a convincing simulation of an executive’s voice. The attack vector is straightforward: call a finance team member, simulate an executive, manufacture urgency, request a wire. The psychological defence that “I’d recognize their voice” is no longer valid and training people to question that instinct, while preserving the efficiency of normal operations, is one of the harder change management challenges Canadian institutions now face.

Machine identity exploitation

It is the threat most Canadian executives have yet to fully reckon with. Financial institutions now operate with more non-human identities: APIs, service accounts, automated agents, third-party integrations, than human ones, and most are poorly governed. Long-lived credentials, infrequent rotation, weak monitoring, and unclear ownership create persistent entry points. An attacker who compromises a machine identity doesn’t need to phish a human being. They already have system-level access, and they can operate quietly for months – automating payment attempts, testing account credentials at scale, or exfiltrating transaction data that will power the next generation of synthetic identity attacks.

Insider Threats

They deserve a separate mention, because they are frequently underweighted in Canadian institutions’ threat models. A privileged employee with access to customer data, transaction systems, or approval workflows represents a fraud risk that external controls alone cannot address. The challenge is that insider fraud is designed to look like authorized activity, because it is authorized, by someone who shouldn’t be authorizing it. User and Entity Behaviour Analytics, a specific application of AI that monitors employee behaviour patterns across systems and flags deviations from established norms, is increasingly essential for institutions that take this risk seriously.

We had a client where the fraud had been occurring for nearly two years before it was detected. A payments operations employee was making small, authorized-looking adjustments to beneficiary account details on a recurring basis. Each individual transaction was within their authorization limits. It was only when an AI system flagged the cumulative pattern – the same employee, the same type of adjustment, the same timing – that anyone looked. By that point, the losses were significant. The lesson is that insider fraud is a patient crime, and patience is exactly what rule-based systems can’t detect.

These four vectors share a design principle: they are built to look like normal activity. Traditional fraud controls were built to catch anomalies. That fundamental mismatch is why they are failing.

What AI Fraud Detection Actually Does

The shift from rule-based fraud prevention to AI-powered detection is often framed as a technology upgrade. It is better understood as a fundamentally different philosophy of defence: one that moves from asking “does this match a known bad pattern?” to asking “given everything we know about this customer, this device, this moment, and this context, does this make sense?”

The difference in detection capability is substantial. AI-based systems have demonstrated the ability to detect two to four times more suspicious activity while reducing alert volumes by more than 60%. For compliance teams drowning in false positives and the review fatigue that generates, that second number matters as much as the first. In practice, modern AI fraud detection operates across four layers that work in concert.

Continuous behavioural monitoring builds a dynamic profile of what normal looks like for each customer – their typical transaction size, their usual locations, their device patterns, their time-of-day behaviour, their navigation cadence within digital banking platforms. When something deviates from that profile in a statistically meaningful way, the system flags it, not because it matches a rule, but because it doesn’t fit the pattern. This is how institutions catch the low-and-slow fraud that deliberately stays beneath static thresholds.

Consider a real scenario: a long-standing customer at a major Canadian bank suddenly initiates three international wire transfers over a forty-eight hour period to accounts in jurisdictions the customer has never transacted with before. The amounts are individually below reporting thresholds. A rule-based system passes all three. A behavioural AI system flags the cluster immediately, not because any single transfer broke a rule, but because the combination represents a complete deviation from eighteen months of established customer behaviour. An analyst reviews, contacts the customer, and discovers they have been the victim of a romance scam. The transfers are halted. The customer’s funds are protected. That outcome is only possible with continuous behavioural monitoring.

Network and relationship analysis addresses the reality that fraud rarely operates in isolation. Organized fraud rings, money mule networks, and synthetic identity operations leave traces in the relationships between accounts, devices, and transactions that no transaction-level analysis would detect. Graph analytics maps these connections in real time, surfacing that five new account applications share a device fingerprint, or that a pattern of payment flows between twelve accounts follows a structure consistent with layering in a money laundering operation, or that a set of loan applications submitted through different branches share underlying data points pointing to a common origination source.

The cases that concern us most are the ones that look perfectly clean at the transaction level. Organized fraud groups are sophisticated enough to ensure each individual touchpoint passes scrutiny. Where they can’t hide is in the network – the relationships between accounts, devices, and behavioural patterns that only become visible when you’re looking at the whole graph rather than individual nodes. That’s where AI creates an asymmetric advantage for the defender.

Real-time identity and document verification

It has become a critical battleground as digital onboarding has expanded. AI systems applying computer vision and deepfake detection can identify forged documents, synthetic selfies, and injected media attacks during the onboarding process, flagging anomalies that human reviewers would miss and that rule-based checks cannot evaluate. Liveness detection has evolved beyond simple movement prompts to identify replayed media, synthetic imagery, and AI-generated faces with a sophistication that keeps pace with the tools attackers are using to generate them.

A practical example: a Canadian digital lender processing high volumes of online applications began seeing a cluster of approvals that subsequently defaulted within ninety days. Post-incident review revealed that a significant proportion had passed standard document verification: government IDs that looked legitimate, selfies that cleared liveness checks, but had been generated using AI tools that had improved faster than the lender’s verification vendor had updated its detection models. The lesson is not that identity verification is futile. It is that it must be continuously updated against the current generation of forgery tools, not the generation that existed when the contract was signed

Autonomous case management

Agentic AI is where the operating model transformation becomes most significant. Rather than simply flagging a suspicious transaction for human review, an agentic system can detect the event, contact the customer through a personalized, contextually appropriate message to verify whether the transaction is legitimate, evaluate the response, and take appropriate action, all within seconds, and all with a complete, auditable record of every step. A customer initiates an unusual large transfer. The system detects the anomaly, sends a personalized verification message referencing the specific transaction, receives a concern flag from the customer, and pauses the transfer pending analyst review before the funds have moved.

For Canadian banks managing thousands of alerts daily, this shifts the analyst’s role from processing volume to handling genuine complexity. Institutions deploying agentic AI in financial crime operations have reported productivity improvements ranging from 200% to 2,000% – not because they replaced their people, but because each person is now doing work that actually requires human judgment.

The Financial Impact: What’s Actually at Stake

Fraud prevention is sometimes discussed in Canadian boardrooms primarily as a compliance cost: something that must be managed to satisfy regulators, rather than an investment with a measurable return. That framing undersells both the risk and the opportunity.

The direct financial exposure is significant and growing. US consumers alone reported over $12.5 billion in fraud losses in 2024: nearly quadruple the $3.5 billion lost four years earlier. Canadian figures follow the same trajectory. A KPMG Canada survey found that 72% of respondents had lost up to 5% of business profits to AI-powered attacks in the previous twelve months alone. For a mid-sized Canadian bank, 5% of annual profit is not a rounding error. It is a material financial event that affects shareholder returns, capital ratios, and the ability to invest in growth.

The indirect costs are equally significant and more difficult to quantify. Fraud losses that become public erode customer trust in ways that take years to recover. Regulatory findings: particularly those involving inadequate detection or reporting of suspicious activity, carry both financial penalties and reputational consequences that affect institutional credibility with regulators, counterparties, and enterprise clients. And in a competitive environment where digital banking experience has become a primary differentiator, the friction created by high false positive rates — legitimate transactions declined, customers asked to verify routine activity carries a measurable impact on retention and lifetime value.

“The ROI conversation for AI fraud detection is actually quite compelling when you model it correctly,” says a Dedicatted financial advisory specialist. “Most institutions are only counting the direct fraud loss reduction. But when you factor in the compliance cost efficiency, the false positive reduction and its effect on customer experience, and the avoided regulatory exposure, the business case strengthens considerably. The institutions that have done that full analysis are not debating whether to invest. They’re debating how fast to move.”

More than 93% of surveyed financial institutions globally are planning to invest in AI in the next two to five years, with fraud detection consistently ranking as the top application. The question for Canadian banking leaders is not whether this investment is coming – it is whether your institution is leading that transition or responding to it.

The Cybersecurity Dimension

AI fraud detection and cybersecurity are not the same function, but the line between them has become meaningfully blurred, and institutions that treat them as entirely separate domains are leaving a significant gap in their defences.

The most sophisticated financial fraud attacks today are hybrid operations. They begin with a cybersecurity breach – a compromised credential, an exploited API vulnerability, a machine identity taken over and then use that access to facilitate financial crime. The attacker who compromises a service account doesn’t immediately drain accounts. They watch. They learn the institution’s transaction patterns, identify the approval workflows, understand which controls exist and how they are monitored. Then they act, in a way specifically designed to avoid triggering those controls.

Addressing this requires that fraud and cybersecurity functions share intelligence in real time, not through periodic reporting cycles. An anomaly detected by the security operations center: unusual API call volumes, a service account accessing data outside its normal scope, a login from an unexpected geography should immediately inform fraud risk scoring for transactions associated with that account or customer. Currently, most Canadian institutions do not have the integration architecture to make that happen automatically.

We’ve done assessments where the security team and the fraud team were both aware of signals that, taken together, would have clearly indicated an active attack. But because those signals lived in separate systems with separate alerting processes and separate escalation paths, neither team had the full picture. The attack succeeded. The integration work to connect those functions isn’t glamorous: it’s plumbing, but it is some of the highest-value risk reduction work we do.

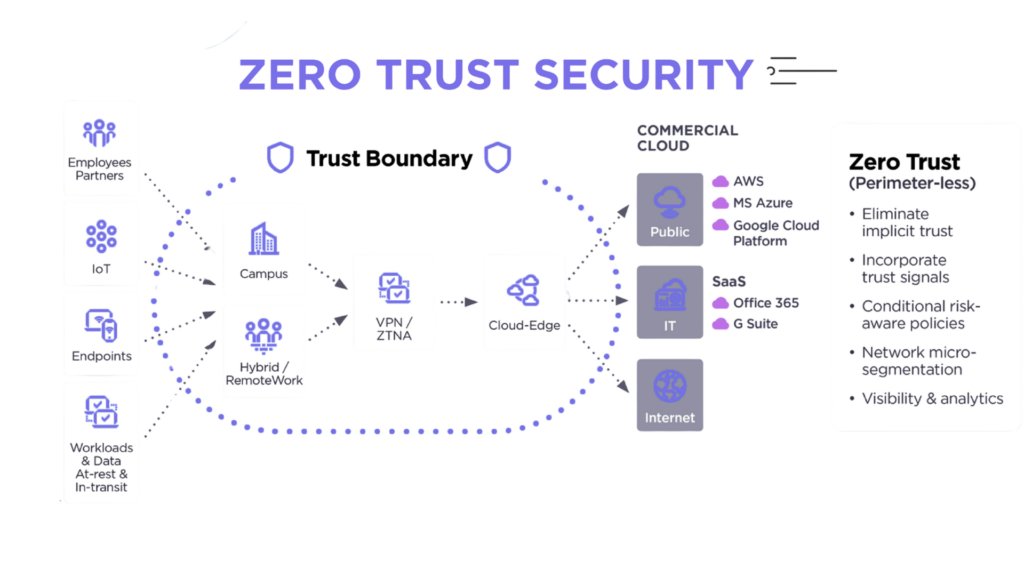

Zero Trust architecture is increasingly relevant in this context. Rather than assuming that entities inside the network perimeter are trustworthy, Zero Trust continuously verifies the identity and integrity of every user, device, and application: before, during, and after they’ve accessed resources. For financial institutions where the perimeter has effectively dissolved across cloud environments, third-party integrations, and remote workforces, Zero Trust provides the architectural foundation on which both cybersecurity and fraud controls can operate with shared intelligence.

AI also introduces its own security considerations that Canadian banking leaders must account for. Agentic AI systems can take autonomous action within financial workflows – represent a new category of attack surface. They can be vulnerable to prompt injection attacks that manipulate their inputs, adversarial examples designed to cause misclassification, and exploitation of the API connections that give them access to core systems. This is not an argument against deploying agentic AI. It is an argument for deploying it with the same rigorous security testing: red teaming, adversarial simulation, privilege boundary enforcement , that any other critical system would require.

The Canadian Compliance Imperative

Technology capability and regulatory compliance are often framed as competing priorities. In the Canadian context, they are increasingly the same requirement and institutions that have not recognized that alignment yet will be forced to by the regulatory environment that is arriving.

FINTRAC’s suspicious transaction reporting regime demands not just that institutions detect financial crime, but that they document the reasoning behind every report and demonstrate that the detection process itself is sound. OSFI’s model risk management guidelines require that AI systems used in risk decisions be validated, monitored, and governed with the same rigour applied to any other risk model. And Canada’s Bill C-27, currently advancing through Parliament, will establish explicit legal requirements for AI explainability: high-impact automated decisions must be explicable to the people they affect and defensible to regulators.

This creates a specific design requirement that many institutions are not yet meeting. An AI fraud detection system that produces accurate results but cannot explain how it reached them is a compliance liability in Canada, not a compliance solution. When a FINTRAC auditor asks why a suspicious activity report was filed or why it wasn’t “the model flagged it” is not an adequate answer.

We talk to compliance officers across the sector who are genuinely excited about what AI can do for their detection capabilities, but they’re nervous about the governance side. And they should take that seriously. Bill C-27 is going to require explainability at a level that a lot of current AI deployments simply cannot provide. The institutions that build that in from the start will have a significant advantage when the legislation comes into force. The ones that retrofit it afterward will have a painful and expensive experience.

Most Canadian institutions believe their AI governance is in reasonable shape. The ones that have actually benchmarked it against OSFI Guideline E-23 often discover otherwise: gaps in explainability documentation, model lifecycle processes that don’t meet the standard, third-party vendor risk that hasn’t been formally assessed. We built a free tool specifically for this: 30 questions across six categories, aligned to OSFI E-23, the EDGE principles, and the AMF AI Guidelines, with a personalized scorecard you can put in front of your board or your next OSFI examiner. It takes ten minutes. The findings usually take longer to sit with. Find out where your institution actually stands with Dedicatted free assessment

The institutions getting this right are building explainability in as an architectural requirement from day one. Every alert comes with a plain-language summary of what triggered it, which features drove the risk score, and what the system’s confidence level is. Every human decision is logged with the analyst’s reasoning. Every model is monitored for performance drift and recalibrated on a documented schedule. The audit trail is not an afterthought – it is the product.

There is also a fairness dimension that Canadian boards are beginning to take seriously. AI models trained on historical data can encode systemic bias: disproportionately flagging certain customer demographics, or using proxy variables like postal codes that reflect socioeconomic patterns rather than genuine risk signals. The institutions monitoring for this proactively will be well positioned when regulators begin requiring documented bias assessments. Those that haven’t will face an uncomfortable conversation at an inopportune moment.

Royal Bank of Canada has publicly discussed its investment in AI-driven compliance infrastructure specifically designed to produce explainable outputs for regulatory review — framing explainability not as a constraint on detection performance but as a core product requirement. That framing is where Canadian banking is heading. The question is whether your institution arrives there by design or by necessity.

People, Judgment, and Accountability: The Human Side of AI Fraud Detection

Every serious analysis of AI fraud detection arrives at the same point: the technology is only as effective as the people and governance structures around it. This isn’t a caveat – it is a design principle that separates institutions realizing value from those that don’t.

AI processes scale, identifies patterns, and moves at machine speed. It does not make the judgment calls that define sophisticated financial crime cases. The customer behaving strangely because they are a victim of elder fraud and need protection, not investigation. The transaction pattern that resembles layering but has a legitimate cross-border business explanation that only a relationship manager would know. The suspicious activity report decision that carries reputational and legal consequences and requires a named human being to be accountable for it. Those decisions belong to people and effective AI fraud detection is designed to surface them to the right people with the right context, not to make them autonomously.

One thing we push back on with clients who want maximum automation is the question of what happens when the system is wrong. And it will be wrong sometimes. The question is whether your organization has built the human oversight layer to catch those cases or whether you’ve automated past the point where a human being is still in the loop when it matters. Getting that balance right isn’t a technology problem. It’s a governance problem.

The practical implication is an organizational design question as much as a technology question. Fraud, cyber, identity, and compliance functions operating in silos cannot mount a coordinated defence against threats operating across all those domains simultaneously. A deepfake wire fraud attempt involves social engineering, identity verification failure, payment controls, and potentially compromised internal communications: touching four different functional owners in most Canadian institutions, none of whom has full visibility. The institutions seeing the best outcomes from AI fraud detection have reorganized around cross-functional teams with shared intelligence, common metrics, and joint accountability for outcomes. The change management challenge is consistently underestimated. Building the technology takes months. Changing how analysts, compliance officers, and relationship managers work with that technology takes longer. Recent Mckinsey surveys found that only 26% of Canadian organizations have a tested, formal fraud incident response plan explicitly covering AI-powered attacks. That gap cannot be closed with technology.That gap cannot be closed with technology. It requires deliberate investment in training, role redesign, simulation exercises, and leadership that treats fraud preparedness as an ongoing operational priority rather than a project with a completion date.

What Good Looks Like: Dedicatted in Practice

Dedicatted took over full Managed Support Services for a global financial technology company operating a cloud-native platform across multiple regions – an environment with the same reliability, security, and compliance demands that Canadian banks running AI fraud detection face every day. The operational gaps were significant: no 24/7 coverage meant incidents occurring outside business hours went unresolved until someone became available, a critical exposure for any platform where fraud doesn’t observe business hours. Infrastructure patch debt had accumulated across EKS clusters and operating systems, precisely the unpatched components that machine identity exploitation attacks are designed to find. And a disaster recovery plan existed on paper but had never been tested. Nobody actually knew whether the platform would meet its recovery objectives when it mattered most.

Under Dedicatted’s MSP model, the platform reached 99.97% uptime with 15-minute P1 response times, rolling patch management eliminating accumulated infrastructure debt, and a full disaster recovery simulation confirming cross-region recovery in under one minute. Security controls and compliance posture were strengthened across SOC 2, ISO 27001, and GDPR requirements – the same compliance framework Canadian banks must demonstrate to OSFI and FINTRAC examiners.

The lesson applies directly: the most sophisticated AI fraud detection capability means nothing if the platform running it goes dark at 2am, or if an unpatched component becomes the entry point for the exact attack the system was built to prevent. Operational resilience isn’t the unglamorous part of fraud prevention. For Canadian banks serious about AI-powered financial crime defence, it is fraud prevention. Want to see exactly how we did it? Read the full case study

What Canadian Banking Leaders Should Do Now

Canadian banking leaders who are still treating AI fraud detection as a technology project are looking at it through the wrong lens. This is a strategic risk question – one that simultaneously touches financial performance, regulatory standing, customer trust, and competitive positioning. The industrialization of fraud means that the gap between institutions with sophisticated AI-powered defences and those relying on legacy controls widens every year, as fraudsters access better tools, accumulate better intelligence on which institutions are easier targets, and refine their approaches based on what has worked before.

Here’s a practical starting point: before your next board discussion on AI fraud detection, know your governance score. Our free OSFI AI Governance Assessment benchmarks your institution against Guideline E-23, the EDGE principles, the AMF AI Guidelines, and the NIST AI Risk Management Framework – the exact standards your regulators are using to evaluate you. It covers the six areas where Canadian banks most commonly have gaps: governance and oversight, explainability and transparency, data quality, ethics and fairness, model lifecycle management, and third-party risk. Thirty questions. Ten minutes. A scorecard that tells you not just where you stand, but what closing each gap would actually require. Take the free assessment and walk into your next board meeting prepared

“We see institutions that have invested seriously in AI fraud detection using it as a differentiator in enterprise client conversations,” notes a Dedicatted senior advisor. “Large corporate clients, high-net-worth individuals: they are asking harder questions about how their bank protects them. The answer ‘we have rule-based transaction monitoring and an alert team’ is not landing the same way it did three years ago.”

The near-term priorities are clear. Audit your actual fraud exposure against today’s threats: synthetic identities, deepfake social engineering, machine identity compromise, insider risk, not against the landscape of five years ago. Invest in data governance before model sophistication, because the most common barrier to effective AI fraud detection is fragmented and inconsistently structured data, not model quality. Design for explainability from the beginning, because Bill C-27’s requirements are coming and retrofitting compliance into AI systems is expensive and often inadequate. Integrate your fraud and cybersecurity functions around shared intelligence, because the most damaging attacks of the next five years will operate across both domains simultaneously. And define the human role explicitly, because AI operating without clear governance boundaries is a liability, not an asset.

Most importantly: treat fraud prevention as what it has become. Not a compliance function that surfaces to the board when something goes wrong. A strategic capability: one that protects revenue, protects customers, satisfies regulators, enables growth, and increasingly differentiates institutions that are serious about the future from those managing the present.

The institutions that will lead Canadian banking in five years are building that capability now. The signal to act arrived some time ago. The question is what your institution is doing with it. At Dedicatted, financial crime prevention is work we do every day: from AML transformation and AI fraud detection architecture to the managed infrastructure that keeps those systems running at the reliability Canadian banking demands. If you want to understand where your institution’s fraud detection posture stands today and what it would take to get it where it needs to be, we’d be glad to start that conversation.

We collaborate closely with financial institutions to design, implement, and continuously improve AI-powered fraud detection systems that are built for performance and compliance from the ground up – explainable outputs, auditable decision trails, human-in-the-loop governance, and the operational resilience to run 24/7 without gaps.

As an AWS Premier Tier Partner with the Generative AI Competency, MSP designation, and a place in the AWS Agentic AI Pilot program, we bring a combination no other Canadian partner holds. We have built and operated agentic AI systems across financial services, healthcare, manufacturing, and SaaS and we understand the specific regulatory expectations Canadian banks face under FINTRAC, OSFI, and the advancing provisions of Bill C-27.

Our team of over 50 AI, Data, and ML experts is ready to map your fraud detection use case, assess your current posture against today’s threat environment, and scope a path forward that is honest about effort, timeline, and cost. Talk to us.